The first official treaty between the United States and China was forged in 1844 under questionable circumstances. In the wake of Britain’s significant successes with the Qing Empire during the First Opium War, the US aimed to secure similarly favorable terms.

This led to the Treaty of Wangxia, signed between an emerging power, the US, and a declining one.

The treaty granted the US entry to five treaty ports (Guangzhou, Xiamen, Fuzhou, Ningbo, and Shanghai), where Westerners enjoyed special privileges such as extraterritoriality, which incited significant anger among the Chinese, as it allowed Westerners accused of crimes to avoid trial by Chinese courts.

Read:

The new superpower test: Who is trusted when fear rises?

Winners and losers from Trump and Xi’s two-day Beijing summit

This initiated a timeframe in China known as the “century of humiliation,” marked by a second Opium War, a Japanese invasion, civil strife, and the communist revolution in 1949.

In sharp contrast, last week’s gathering between Presidents Donald Trump and Xi Jinping in Beijing unfolded in a much friendlier atmosphere, resulting in affirmations of camaraderie and cooperation.

Nonetheless, deep-seated tensions linger.

Presently, China is the resurgent power challenging the US’s status as the singular global superpower. China forges strong alliances with Russia, opposing Western support for Ukraine, while being Iran’s main trade partner.

Taiwan remains a significant point of dispute, with China staunchly promoting eventual reunification, while the US supports the existing status quo.

The vital role Taiwan plays as the world’s leading producer of advanced semiconductors places it at the forefront of the artificial intelligence (AI) boom, complicating the situation further.

Read:

Taiwan market cap tops $4trn on AI boom, overtaking UK

Global chip stocks soar as Huang helps ignite AI excitement at Davos

The US has been striving to maintain its edge in AI and other technologies by limiting China’s access to high-end chips. In contrast, China excels in various technologies associated with the green transition, being the top producer of solar panels, batteries, wind turbines, and electric vehicles.

Essentially, it parallels being the Saudi Arabia of clean energy, and considering AI’s heavy electricity demands, this might eventually provide it with a competitive advantage.

China also dominates 80% to 90% of the global supply of various “rare earth” minerals, crucial for a range of military and industrial technologies, granting it considerable bargaining leverage in negotiations with any nation, including the US.

The world’s factory

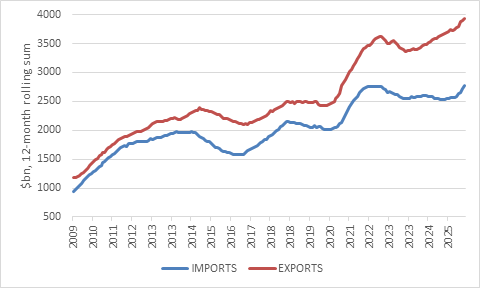

Indeed, China is overwhelmingly the largest manufacturer of numerous goods essential to global markets, covering both basic and advanced technologies. As a result, its trade surplus (exports minus imports) has reached unprecedented heights, surpassing $1 trillion last year.

This narrative suggests echoes from the past.

The Opium Wars forced China to accept drug imports from Britain and other colonial powers.

Read:

US-China trade truce leaves fundamental issues unresolved

A Supreme Court showdown looms for Trump’s tariffs

China confronts contradictions

While the Western world sought Chinese products, the reverse was not true, leading to a significant outflow of gold and silver to the east [as China accepted payment solely in precious metals]. Additionally, the imposition of opium on China—after colonial powers had addicted its populace—had devastating social ramifications and was a strategy to address the severe trade imbalance.

Similarly, Trump imposed tariffs on China during his initial term to tackle the modern trade deficit, a strategy that his successor, Joe Biden, largely upheld.

Hardline approaches to China have emerged as a rare bipartisan concern in Washington.

ADVERTISEMENT

CONTINUE READING BELOW

Consequently, exports from China to the US have substantially decreased. At its peak in 2017, nearly a quarter of US goods imports by value stemmed from China.

By April of this year, that percentage had plummeted to just 8%, although some might still be routed through third countries like Vietnam.

While much of the world has not mirrored Trump in raising trade barriers against China, it doesn’t mean they aren’t keen to.

Industries across Asia, Europe, and beyond are facing considerable pressure from Chinese imports, with the automotive sector particularly hit as China transitioned from a car importer to the largest exporter by volume in recent years.

China’s exports and imports by value

Source: LSEG Datastream

This strong export performance, alongside a notable decline in imports, indicates a shift towards domestic brands.

However, the trade surplus also conceals a weakness: a lack of domestic demand. This is partly a result of conscious policy choices.

China’s economic model is widely recognized for favoring investment over consumption, leading to households retaining a smaller portion of national income compared to countries at a similar development stage.

Significant resources have flowed into the development of world-class infrastructure and manufacturing capabilities. Nevertheless, a considerable share of this investment was directed towards residential real estate, culminating in a significant bubble that burst in 2022.

The aftermath of the property bubble continues to resonate throughout the economy. A drop in apartment sales translates to fewer purchases of fridges, televisions, and beds, many of which would have been imported.

If imports had matched exports, Chinese consumers could have obtained an additional $100 to $200 billion worth of foreign goods.

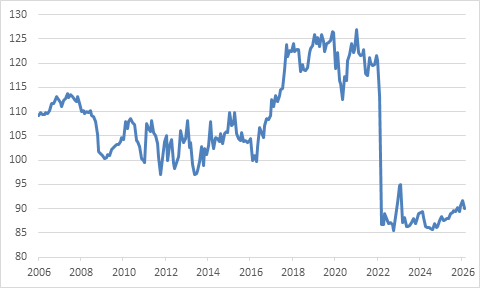

Instead, consumer confidence remains at a historic low, albeit slightly improved compared to a year prior.

Chinese consumer confidence

Source: LSEG Datastream

Yuan too few

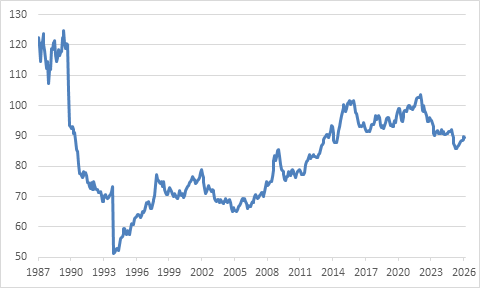

Another reason behind the weakness in imports—and strength in exports—is an undervalued currency, a long-standing issue for the US government.

In most cases, a nation with such a substantial trade surplus would typically experience upward pressure on its currency. Even with some recent gains, the yuan remains relatively weak on a real trade-weighted basis.

China real trade-weighted exchange rate

Source: OECD

A weak currency generally bolsters exports and restricts imports, which is why Trump advocates for a softer dollar and a stronger yuan.

ADVERTISEMENT:

CONTINUE READING BELOW

A shift of this nature would help balance the trade dynamics between China and the rest of the world while enhancing the purchasing power of Chinese households, allowing for more foreign goods, services, and travel abroad.

The yuan’s exchange rate is managed by the People’s Bank of China (PBOC), making its level a conscious decision rather than an inevitability.

While it seems prudent for the yuan to appreciate gradually over time, the PBOC typically prioritizes stability above all else.

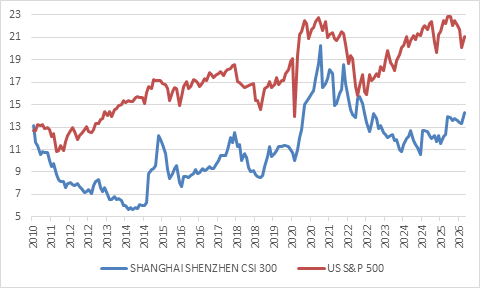

Next, let’s compare the equity markets of the US and China. Although China can assert itself as a formidable economic, military, and technological superpower, market valuations convey a different story.

Conversely, despite discussions about US decline during Trump’s erratic presidency, the S&P 500 has consistently achieved new heights, even amid ongoing geopolitical tensions.

Forward price-earnings ratios

Source: LSEG Datastream

Chinese equities are trading at a substantial discount compared to their US equivalents, especially considering that the yield on a 10-year US government bond was just under 4.5% last week, whereas China’s equivalent was a mere 1.7%. This signifies a significant ‘equity risk premium’ in Chinese stocks while US equities show little margin of safety.

Part of this disparity can be linked to unpredictable regulatory shifts that led to China being labeled “uninvestable” around 2021. Nevertheless, since then, authorities have altered their approach towards Chinese equity markets.

Historically, Beijing viewed equity markets as secondary, believing speculation was less crucial than funding economic growth via the banking system. However, banks now face constraints due to a challenging property sector, and the successes of other countries, especially the US tech sector, have demonstrated how equity markets can facilitate innovation and business growth while simultaneously generating wealth for households—an essential aspect in a nation facing an aging population and uneven social security coverage.

Therefore, regulators are now striving to foster a “slow bull market” with steadily rising equity values to stimulate economic expansion and assist Chinese families in saving for retirement.

To achieve this, corporate governance standards have been enhanced, and publicly listed companies are encouraged to distribute regular dividends, reflecting a significant shift towards a more shareholder-friendly environment.

Despite China’s impressive economic accomplishments, publicly traded companies have struggled to translate GDP growth into profit growth, resulting in lackluster equity returns. In contrast, the primary reason the S&P 500 commands a premium likely resides in its consistent growth in earnings per share, surpassing other major markets.

The profitability of China’s industrial firms has been further affected by overcapacity and vigorous competition, issues policymakers are currently seeking to address through “anti-involution” initiatives.

For equity investors beyond China’s borders, the combination of a depreciated currency, low valuations, and increased policy support is likely to be enticing.

China’s representation in the main global equity indexes compiled by organizations such as MSCI and FTSE Russell has declined to approximately 3%, a figure that does not align with its contribution to global economic output and innovation.

However, risks continue to loom.

China’s concerning demographic situation is widely recognized, primarily as a consequence of the now-defunct one-child policy. Last year, only 7.9 million newborns were recorded, the lowest figures since the Communist Party took power in 1949.

ADVERTISEMENT:

CONTINUE READING BELOW

Read: China’s population grew older and richer … [Jun 2023]

While life expectancy has significantly improved—now exceeding that of the US, an extraordinary achievement—this does not alleviate workforce shrinkage and will inevitably constrain long-term GDP growth rates (ultimately, for equity investors, profits take precedence over GDP).

This trend may also prompt innovation and technological adoption.

According to the International Federation of Robotics, China accounted for half of the world’s industrial robot installations in 2024, with most supplied by domestic firms for the first time.

China’s approach to artificial intelligence appears to focus on practical applications rather than the pursuit of leading-edge models, in stark contrast to Silicon Valley’s winner-takes-all philosophy.

Time will determine the effectiveness of either approach.

Total debt-to-GDP ratios

Source: Bank for International Settlements

A significant concern involves the high total (encompassing household, government, corporate, and financial sector) debt levels, exceeding those of the US when viewed as a percentage of GDP. Notably, the growth rate of this debt is evidently unsustainable.

China holds a significantly higher savings rate than the US or any other large economy, with most of the debt being domestic.

This implies the challenge lies more in internal distribution than in existential crises. Nevertheless, in a slowing economy, servicing this debt becomes daunting, and someone must shoulder the ensuing losses.

A considerable risk exists in the US-China relationship.

Both nations are actively working to lessen their dependency on one another, with China potentially holding a slight advantage. However, their economies remain deeply interconnected, making complete decoupling an unrealistic expectation.

As such, a sharp rupture over Taiwan or other flashpoints could trigger a significant market downturn, affecting markets globally, not just within China.

If the US were to impose sanctions on China, any financial institution would have to comply or risk exclusion from the dollar system.

The US retains substantial leverage in this regard, a fact well understood by China.

A conflict would be detrimental for all parties involved, making last week’s summit between Trump and Xi essential, despite no groundbreaking policy alterations or resolutions on contentious issues emerging from it.

Read:

China will open its market to AI chips from the US, Nvidia’s CEO says

Xi urges Hormuz reopening in rare call with Saudi de facto ruler

US says China agrees to spend billions on agricultural goods

While friendly overtures do not resolve deep-seated disputes, they ensure communication lines remain open. The strategic rivalry between the world’s superpowers is unavoidable, but it can be managed.

Ultimately, both parties—and the entire world—stand to lose if this rivalry escalates into outright conflict.

Izak Odendaal is an investment strategist at Old Mutual Wealth.